Which Firms Are Really Driven by Financial Planning?

June 21, 2022

By Jon Henschen, ThinkAdvisor

What You Need to Know

- While consultative selling and financial plan-driven investing have grown dramatically, they are not as widely practiced as you may think.

- All investment decisions should be backed by some form of financial plan, but often they are not.

- Product-driven investing is increasingly being forced out, largely by FINRA fines.

In 1989, I obtained a securities license through the penny stock firm J.W. Gant, with penny stock firms a common avenue for getting your securities license at the time. These firms were heavily sales driven, with every representative having the book “The Closer” on their desk. (Think of the movie “Boiler Room.”)

One week after getting licensed and observing the representatives at this firm, I left for a sounder financial services foundation to build upon.

To a large degree, sales techniques are tactics that need to be deployed when you lack a person’s trust. Surprisingly, sales tactics and product selling are still heavily utilized while consultative selling and financial plan-driven investing, although having grown dramatically, are not as widely practiced as you may think.

Between Regulation Best Interest and the fiduciary standard, technically all investment decisions should be backed by some form of financial plan, but oftentimes they are not. Captive insurance broker-dealers, wirehouses, banks and transactional stock and bond broker-dealers are still common training grounds for teaching aggressive sales techniques and leading with products to be sold.

As an advisor at a captive insurance broker-dealer explained to me, “I want to grow into wealth management while my broker-dealer is in lockstep with sales of insurance products.”

Industry Divergence

Herein lies a divergence within insurance broker-dealers, with some such as Lincoln Financial and MassMutual being planning driven and having high numbers of certified financial planners, as well as reps with CLU and ChFC designations, yet others we’ve researched falling flat.

In doing an analysis of a well-known captive insurance broker-dealer with over 6,500 representatives, we counted 289 representatives with CFP designations and of those, only about half the CFPs were doing advisory business. That equates to one-half of 1% of their representatives having a CFP designation, and a quarter of 1% that have the CFP designation that are also doing advisory business.

As some insurance broker-dealers resist the conversion to being financial planning driven, independent broker-dealer management increasingly discerns advisors that don’t do financial planning as problematic.

One advisor shared this about joining an independent broker-dealer and his conversation with the president of IBD. The advisor commented, “Your broker-dealer has some of the best brokers in the industry!” The president responded, “That’s the problem, they’re brokers!”

What the broker-dealer president was insinuating was that these representatives were sales driven rather than planning driven. When you have investment decisions motivated by a financial plan, you have an advisor that is largely insulated from conflicts with clients and compliance departments, while product-driven sales can be fertile grounds for customer complaints, such as claims of inappropriate investments or a failure of fiduciary duty.

The Wirehouse Scene

In a recent conversation with an independent RIA, I was reminded how sales driven some wirehouse advisors continue to be. The RIA operated a model that supplied office space, technology and staff for advisors, paying a 65% payout.

Logically I replied, “You must target wirehouse advisors wanting to go RIA?”

There was a long pause, and then he responded, “No, we don’t target wirehouse advisors.”

“Why not?” I asked.

He responded, “They are too salesy for us.” This RIA is financial-planning driven and adheres to a fiduciary standard.

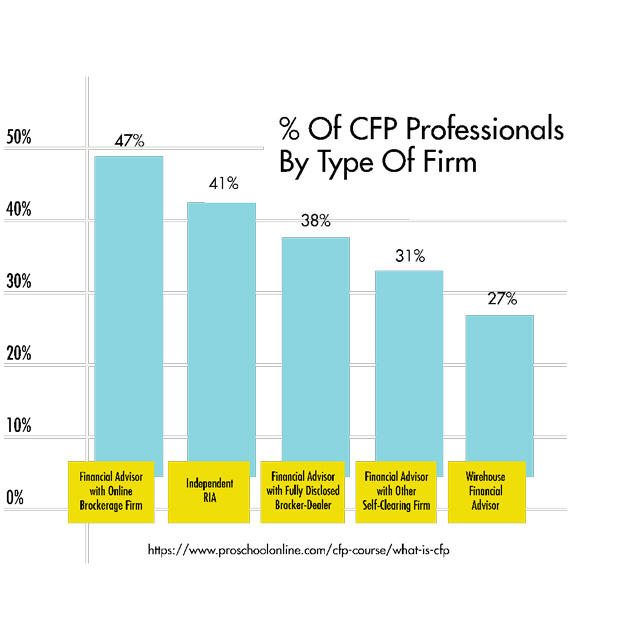

Here’s how the wirehouses rank compared with other advisors channels in terms of CFP percentages:

Fifteen years ago, I read an article ranking financial plans from best to worst. It listed one of the wirehouse firms as having the “worst of financial plans researched, akin to a boiler plate plan,” while a large national firm with both independent and employee reps was seen as “better and more comprehensive but … biased to insurance products;” a firm with only independent advisors was considered “most comprehensive, [by] going into great detail and [being] balanced in recommendations.”

I was curious to know if things had changed much, so I asked blogger Michael Kitces to share his thoughts on the matter. He has done a very detailed analysis, “How Financial Advisors Really Do Financial Planning,” which you can find on his website.

From the research paper, Michael highlighted the following regarding financial planning and the different channels:

- Broker-dealers are most likely to treat their financial planning software like nothing more than a big calculator to estimate a need/gap to sell a product into, while both RIAs and insurance companies are the most likely to customize the financial plan (Figure 17 in Michael’s research paper).

- Insurance companies tend to have the broadest-reaching, “most comprehensive’” financial plan … primarily because they tend to actually cover the full range of the financial plan, while RIAs are less likely to cover the insurance side and broker-dealers tend to be narrower all around.

- Both RIAs and insurance companies tend to spend more time on financial plans, while broker-dealers average almost 25% less time invested into each plan (Figure 19).

- The business model has a big influence on how much time and effort advisors put into producing a quality financial plan.

Michael further explains: “Those on the AUM and commission-based models are quite similar in how much time they invest into a financial plan; but those on the retainer model tend to put almost 30% more time into each plan than those who are AUM or commission-based, and hourly advisors put in more that 10% more time than retainer-based advisors. …

“Depending on your cynical perspective, this is either because hourly advisors ‘run the clock’ due to the fact they’re paid by the hour, or that AUM and Commission advisors give plans short-shrift because in the end they’re paid for by products or portfolios and not advice,” he explained.

Room for More Change

The last five years have seen a huge transformation as product-driven investing is increasingly being forced out, largely by FINRA fines. It has been four years since our recruiting firm received a call from a transaction-focused representative explaining to us that they are active stock traders.

This was one of the most egregious types of investing, and it’s largely been shut down. But we still get calls from advisors with 90%-plus of their book in variable annuities or fixed indexed annuities, selling the principal protection guarantees they offer.

Our industry has improved greatly with the public the beneficiary, but there continues to be room for improvement.

Jon Henschen is founder of Henschen & Associates, a recruiting firm that matches advisors’ needs to best fit broker-dealers and RIAs.